Nonstationary Series

2025-10-15

Nonstationary Series

Nonstationary Series

- Introduction:

- Key Questions:

- What is nonstationarity?

- Why is it important?

- How do we determine whether a time series is nonstationary?

What is nonstationarity?

Recall from earlier part on stationarity:

- Covariance stationarity of y implies that, over time, y has:

- Constant mean

- Constant variance

- Co-variance between different observations that do not depend on that time (t), only on the “distance” or “lag” between them (j):

\(Cov(Y_t,Y_{tj})= Cov(Y_s,Y_{s+j})= \gamma_j\)

Thus, if any of these conditions does not hold, we say that \(y_t\) is nonstationary:

There is no long-run mean to which the series returns (economic concept of long-term equilibrium)

The variance is time-dependent. As time goes on, the variance of the series increases or decreases.

Theoretical autocorrelations do not decay, sample autocorrelations do so very slowly.

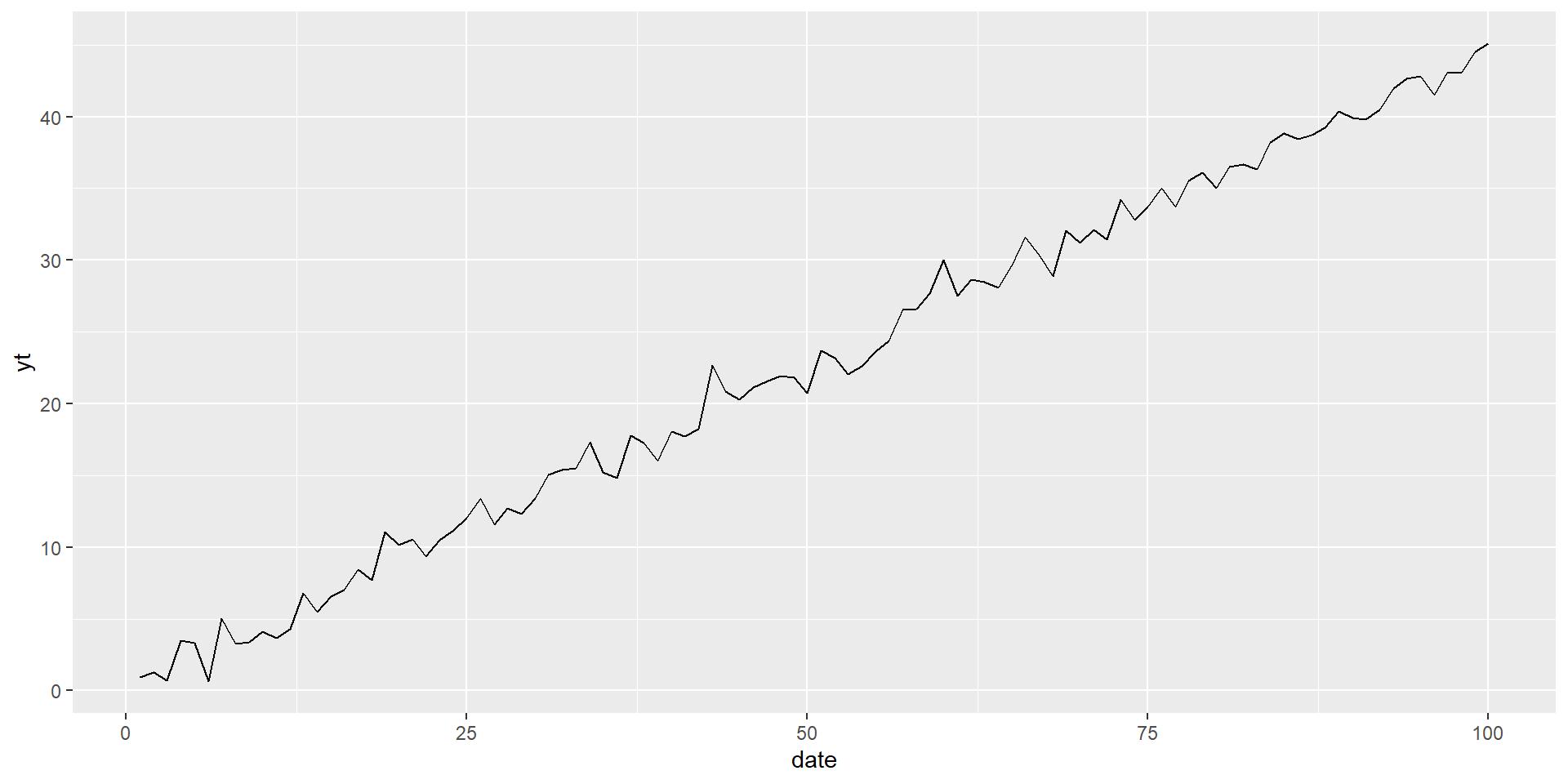

Nonstationary series can have a trend:

- Deterministic: nonrandom function of time:

\(y_t=\mu+\beta t+u_t\) , where \(u_t\) is “iid”

- Example \(\beta=0.45\)

Non-stationary series can have a trend:

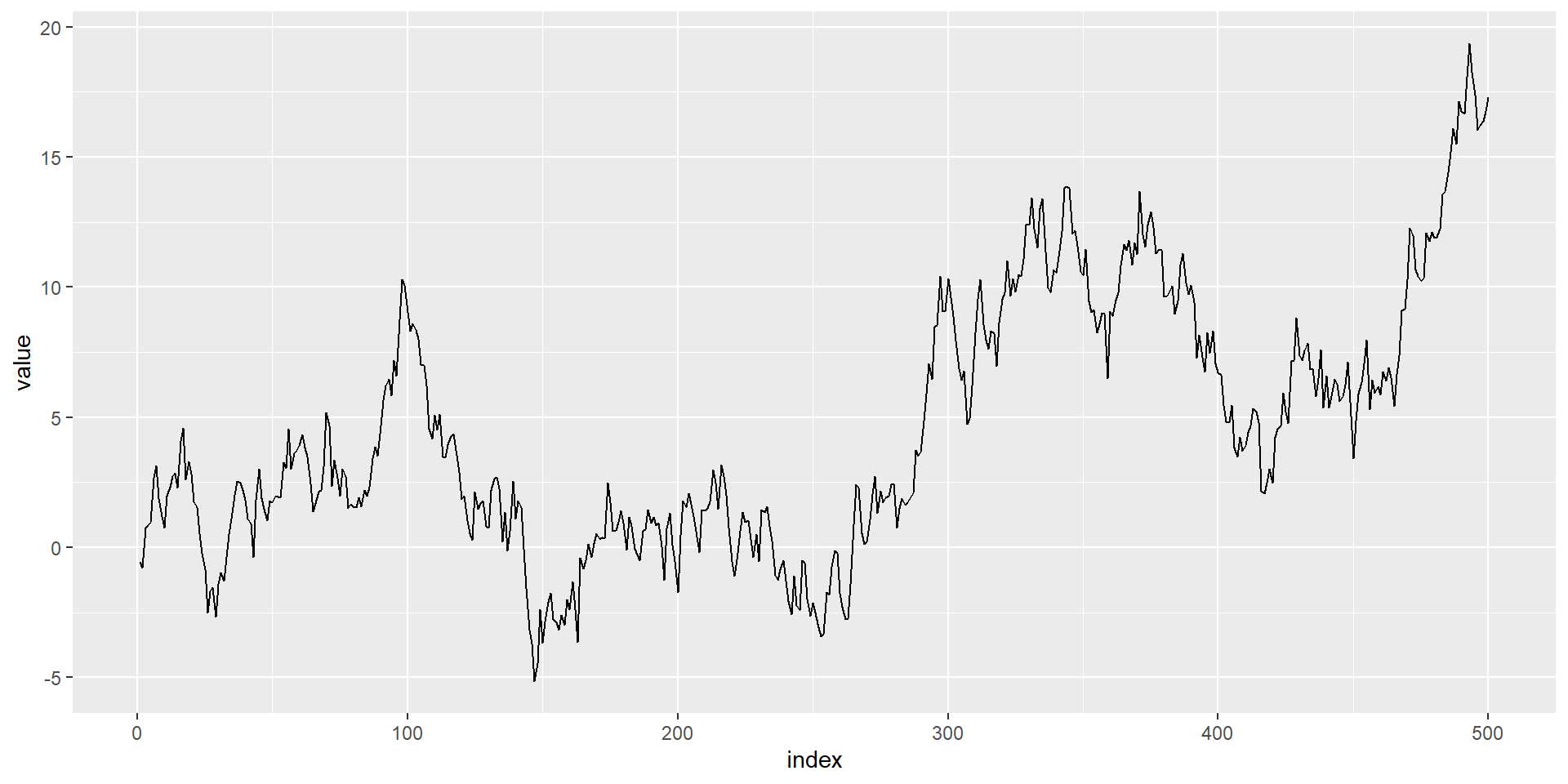

Stochastic: random trend, varies over time

Random Walk: \(y_t=b y_{t-1}+\epsilon_t\)

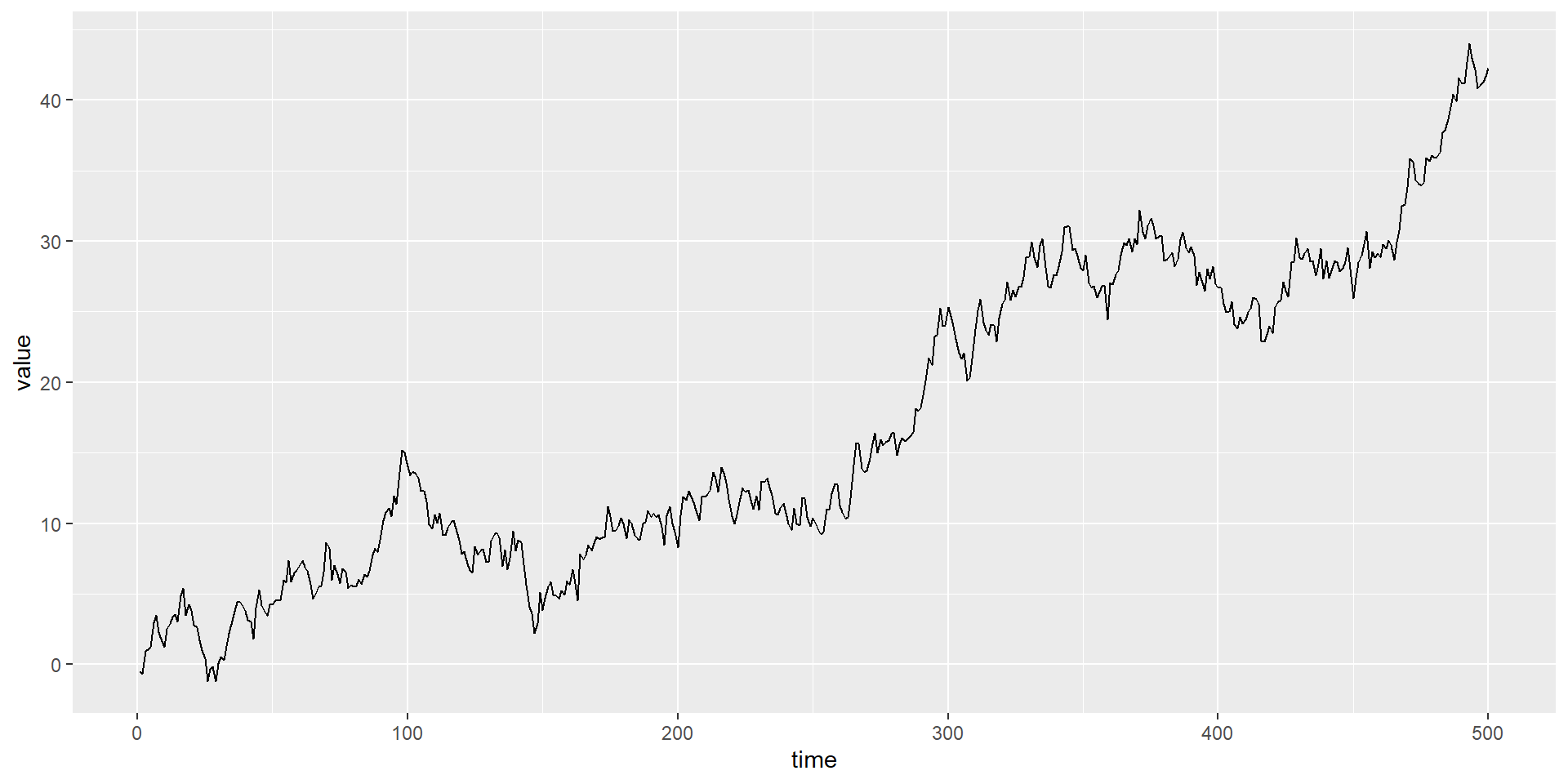

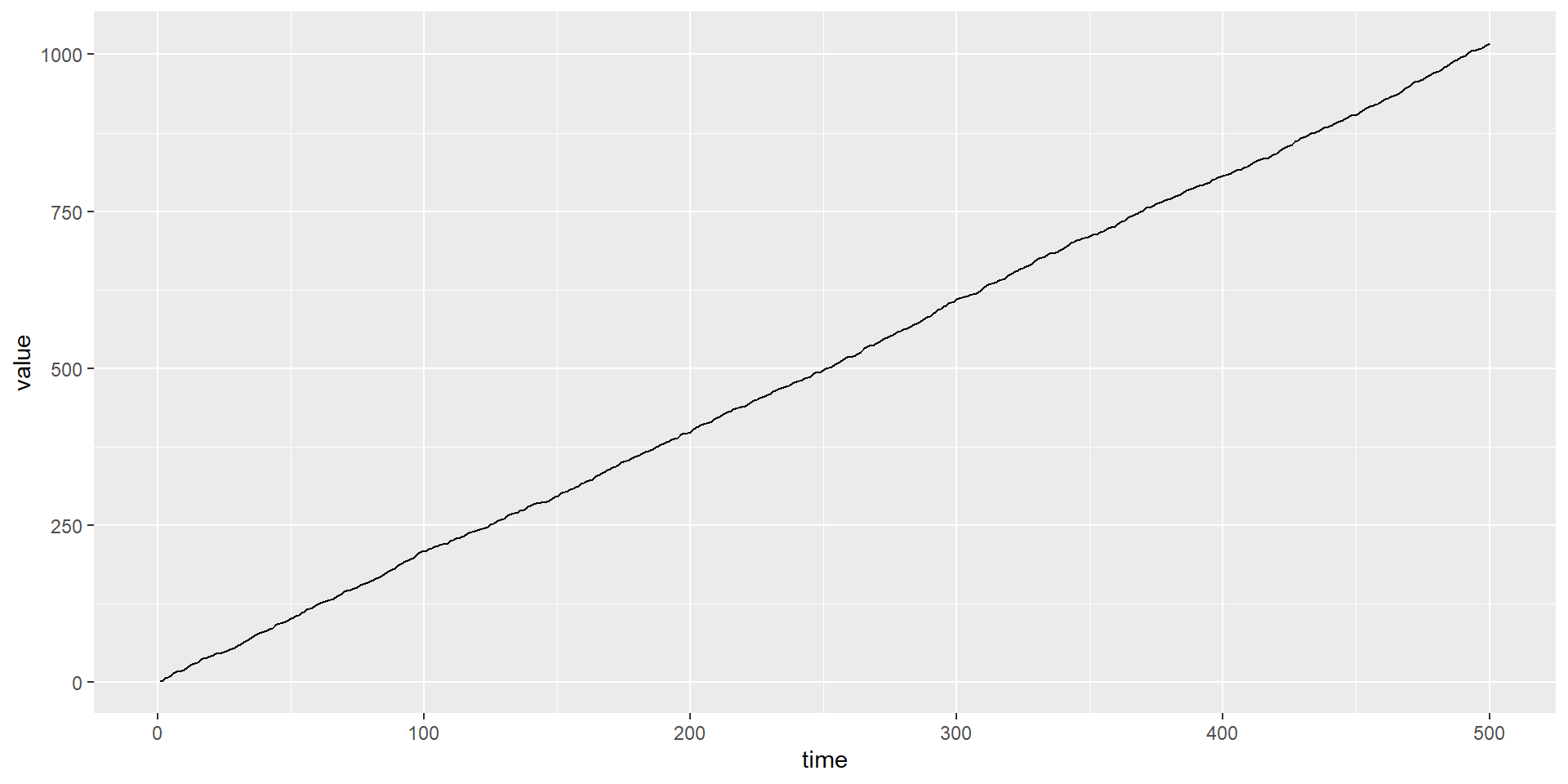

Random Walk with Drift: \(y_t=\mu+y_{t-1}+\epsilon_t\) (as before, \(\epsilon_t\) is iid)

\(\mu\) is the “Drift”;

if \(\mu>0\), then \(y_t\) will be increasing

Question: RW is a special of what process?

Example of a random walk

RW with Drift=0.05

RW with drift is 2

Key Questions:

What is nonstationarity?

Why is it important?

How do we determine whether a time series is nonstationary?

Consequences of non-stationarity

Shocks do not “die out”

Statistical consequences

Non-normal distribution of test statistics

Bias in AR coefficients; poor forecast ability

Shocks do not die out

- Consideer a general AR(1): \(y_t=b y_{t-1}+\epsilon_t\)

- Can be expressed as an MA(q): \(y_t=b^t y_0+\epsilon_t+b\epsilon_{t-1}+b^2\epsilon_{t-2}+. . .+\\b^{t-2}\epsilon_2+b^{t-1}\epsilon_1\)

The impact of shocks (disturbances) will depend on values of \(b\).

\(y_t=b^t y_0+\epsilon_t+b\epsilon_{t-1}+b^2\epsilon_{t-2}+. . .+\\b^{t-2}\epsilon_2+b^{t-1}\epsilon_1\)

Three cases

\(b<0\), \(b^t\) →0 as \(t\) →∞ , so the effects of a shock will diminish as time elapses

\(b=1\), \(b^t=1\) for all t; effect persists, \(y_t=y_0+\sum_{i=1}^{n}\epsilon_{t-i}\) variance grows indefinitely with time.

\(b>1\), shocks become more influential over time.

Statistical consequences of nonstationarity

Non-normal distribution of test statistics

Bias in autorregressive coefficients (b’s);

we might mistakenly estimate an AR(1),

deficient forecast

Usual confidence intervals for coefficients not valid

Statistical consequences of non-stationary for multivariate regressions

For example, two unrelated nonstationary series \(y\) and \(x\) might appear to be related through a standard OLS regression

Hight \(R^2\)

t-statistics that appear to be siginficant

The true test: are the regression residuals stationary? (i-e., long-run equilibrium relationship between \(y\) and \(z\))

Spurious regression practical exercise:

Simulate two random walk series: \(y\) and \(z\) (each with its two disturbances, and either can have drift or not)

- Note by construction, they are unrelated

- Run OLS regression of \(y\) on \(z\), evaluate coefficients, \(R^2\), and plot residulas

Key Questions:

What is nonstationarity?

Why is it important?

How do we determine whether a time series is non- stationary?

Testing for non-stationarity

Recall AR(1) model: \(y_t=by_{t-1}+\epsilon_t\)

Special case: RW, when \(b=1\)

Sationarity requires \(b<1\)

Generalizing to AR(p) :

- Roots of the polynomial below must all be \(>1\) in abs value \(1-b_1Z-b_2Z^2-b_3Z^3-\dots -b_pZ^p\)

If one of the roots=1, then y is said to have a unit root

AR(1) model : \(y_t=by_{t-1}+\epsilon_t\)

Can test for whether \(y\) is a driftless random walk:

\(H_0: b=1\) Or, equaivalently: \(\Delta y_t=\Psi y_{t-1}+\epsilon_t\), \(\Psi=b-1\)

\(H_0: \Psi=0\) - This the ‘Dickey-Fuller’ (DF) test: - Regress \(\Delta y\) on its lag, test for significance of coefficient.

Can extend simple DF test in previous slide:

- Intercept: \(\Delta y_t=\mu+\Psi y_{t-1}+\epsilon_t\)

- Intercept and time trend: \(\Delta y_t=\mu+\Psi y_{t-1}+\alpha t+\epsilon_t\)

- In all three cases, \(H_0:\Psi=0;\) \(y\) has a unit root

Rejecting the unit root test =

find that \(y\) is stationary

Note: critical values for the \(t-statistics\) of \(b\) will vary depending on whether intercept, trend are included.

Some terminology

- Order of integration: number of times a series \(y\) must be differenced to become stationary

- Thus, if \(y\) is “integrated of order zero”, \(I(0)\), then it is stationary (no differencing needed).

- That is, it is stationary in levels

- If \(y\) is \(I(1)\), then its first difference (\(\Delta y\)) is stationary \(\dots\) and so on \(\dots\)

Moving beyond white noise disturbances

DF test assumes that \(\epsilon_t\) is white noise.

However, if \(\epsilon_t\) is autocorrelated, need different version of the test, allowing for higher-order lags:

Augmented Dickey-Fuller (ADF) test:

\(\Delta y_t=\mu+ \gamma y_{t-1}+\sum_i^p \beta_i\Delta y{t-i+1}+\epsilon_t, \gamma=-(1-\sum_i^pb_i)\) and

\(\beta_i=-\sum_i^pb_j\)

ADF test

As with DF, ADF tests whether coefficient on \(y_{t-1}(\gamma)\neq0\)

Must make choices

Intercept, trend, both, none?

p: how many lags? (test statistics are very sensitive to p) - AIC - SBC - General-to-specific (start out with large p, then re-estimate with successively smaller p)

DF, ADF have been found to have low power in certain circumstances:

Stationary processes with near-unit roots

– For example, difficulty distinguishing between \(b = 1\) and \(b = 0.95\) , especially with small samples.

Trend stationary processes

So alternative tests have been designed.

Phillips-Perron (PP) Test:

- Formulation: \(\Delta Y_t=\mu^*+\delta^*t+\Psi y_{t-1}+u_t\) where \(u_t\) is I(0) and may be hetroscedastic and autocorrelated, that is following an ARMA(p,q).

- \(H_0: \Psi=0\)

- PP corrects for any serial correlation and heteroskedasticity in the errors ut by directly modifying the test statistics.

- One advantage of PP: no need to specify lag length.

Kwiatkowski–Phillips–Schmidt–Shin (KPSS)Test:

Null hypothesis: \(y_t\) is trend stationary

Formulation: \(y_t=\beta_0 D_t+\mu_t+u_t\) \(\mu_t=\mu_{t-1}+\epsilon_t\)

Where \(D_t\) contains deterministic components (constant or constant plus time trend), \(\mu_t\) is a random walk

\(H_0: \sigma_{\epsilon}^2=0\)

\(H_1: \sigma_{\epsilon}^2>0\)

KPSS critical values are obtained by simulation methods.

A few notes: A few notes: - DF, ADF, and PP are called “unit root tests”; the null hypothesis is that yt has a unit root; is I(1) or higher.

KPSS, on the other hand, is a “stationarity test”, null hypothesis is that yt is I(0).

Correct specification is key: intercept and trend should be included when appropriate.

Structural breaks can complicate matters further.

A unified way of looking at the unit root tests Slightly different representation: \(y_t=\mu+\alpha t+ u_t\) \(u_t=\rho u_{t-1}+\epsilon_t\)

\(H_0: =1\) y has a unit root

\(H_1: |\rho|<1\) y is stationary

- If \(\epsilon_t\) is white noise, then DF can be used

- If \(\epsilon_t\) is ARMA(p,q) then use ADF or PP

Simulate three processes:

Stationary process with near-unit roots

Trend stationary process

An I(1) process

Graph them and observe their behavior

Conduct Unit Root/Stationarity Tests on all three.

In “Simulated Times Series Examples.xlsx”

Simulate an I(0) process with a structural break

Import into R

Graph and observe

Conduct Unit Root/Stationarity Tests

Now let’s work with real world data

Choose a series:

Look at graph and correlogram for a specific time series

Does it appear to be non-stationary? Does it appear to have a trend, or a structural break?

Undertake Unit Root/Stationarity Tests

Do the different tests agree?

If you suspect a structural break, re-test for two sub-samples