Growth on Hold? Questioning the Logic of Prolonged Stabilisation

Balancing short-term macroeconomic control with the long-term need for structural investment

2025-07-11

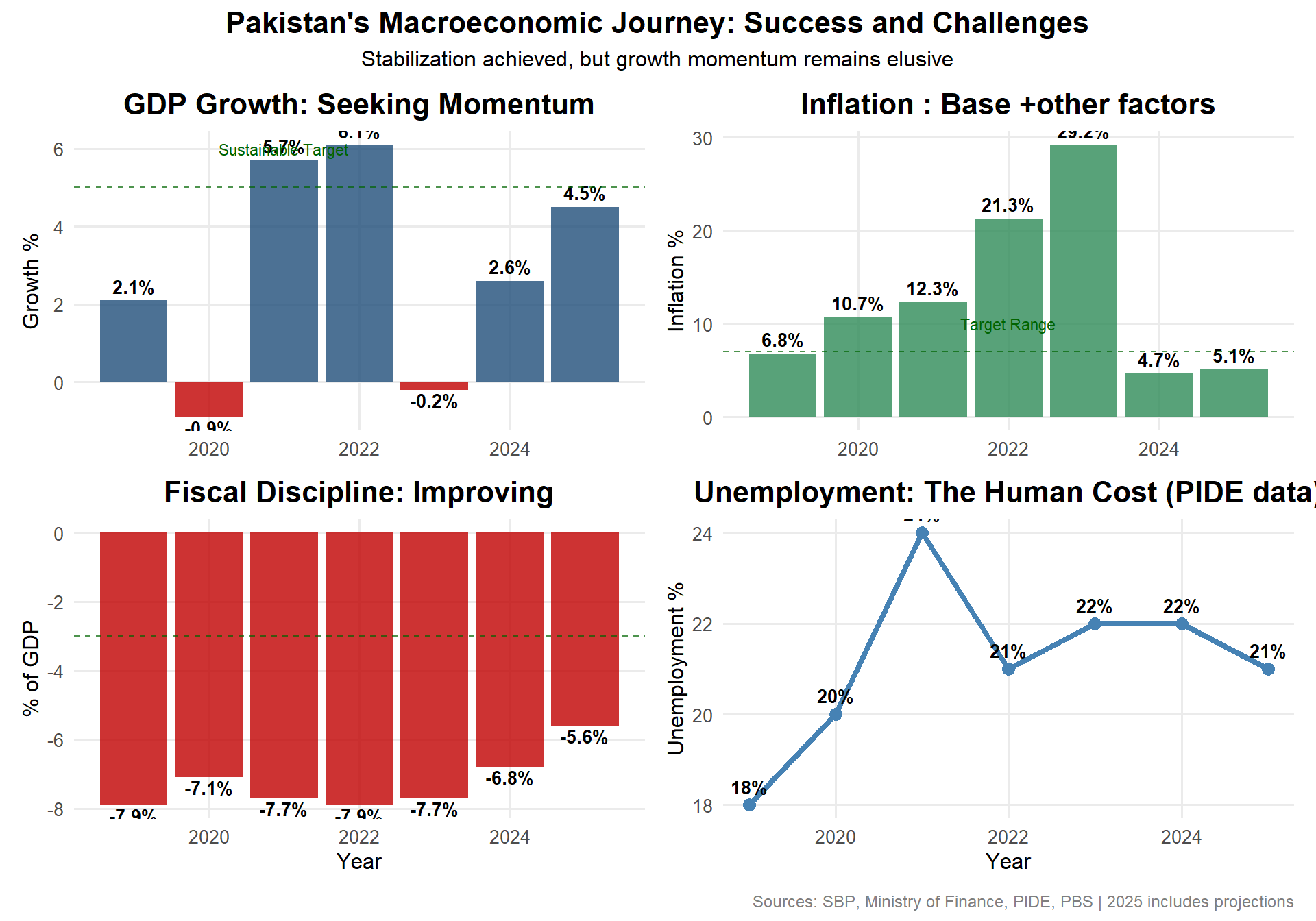

Pakistan’s Economic Transformation: The Numbers Tell a Story

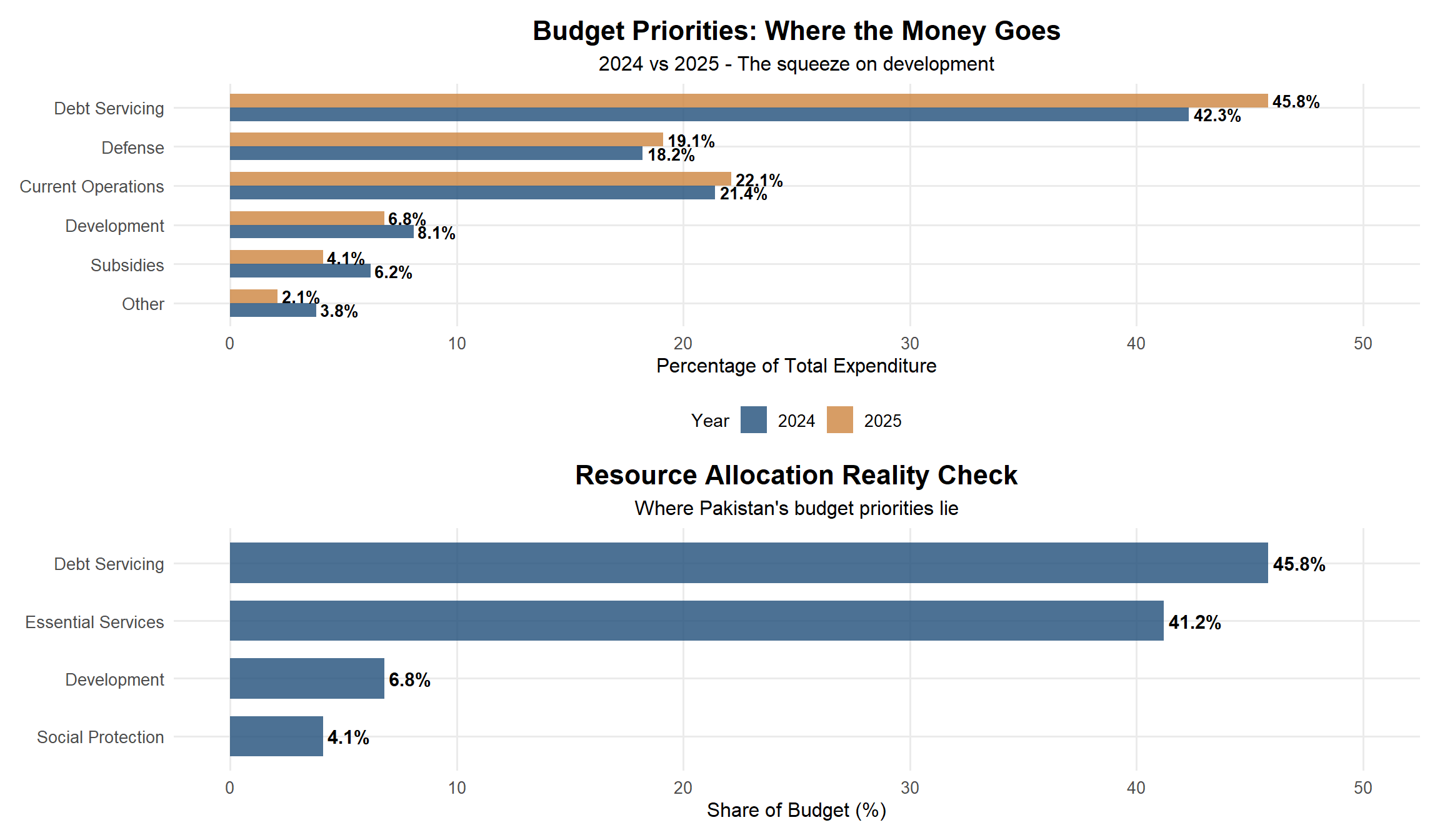

Budget 2025: Stabilization at What Cost?

The Budget’s Message

- What it emphasizes: IMF targets, fiscal discipline, debt management

- What it marginalizes: Development investment, job creation, productivity enhancement

- What it reveals: A budget for survival, not transformation

Tax System & FBR Crisis

FBR

- Single-handedly shrunk formal sector over 15-20 years

- SUPER tax: Don’t grow

- Excessive discretionary powers scaring genuine investors

- Boosted informal economy which doesn’t contribute to productivity, revenues, or FDI

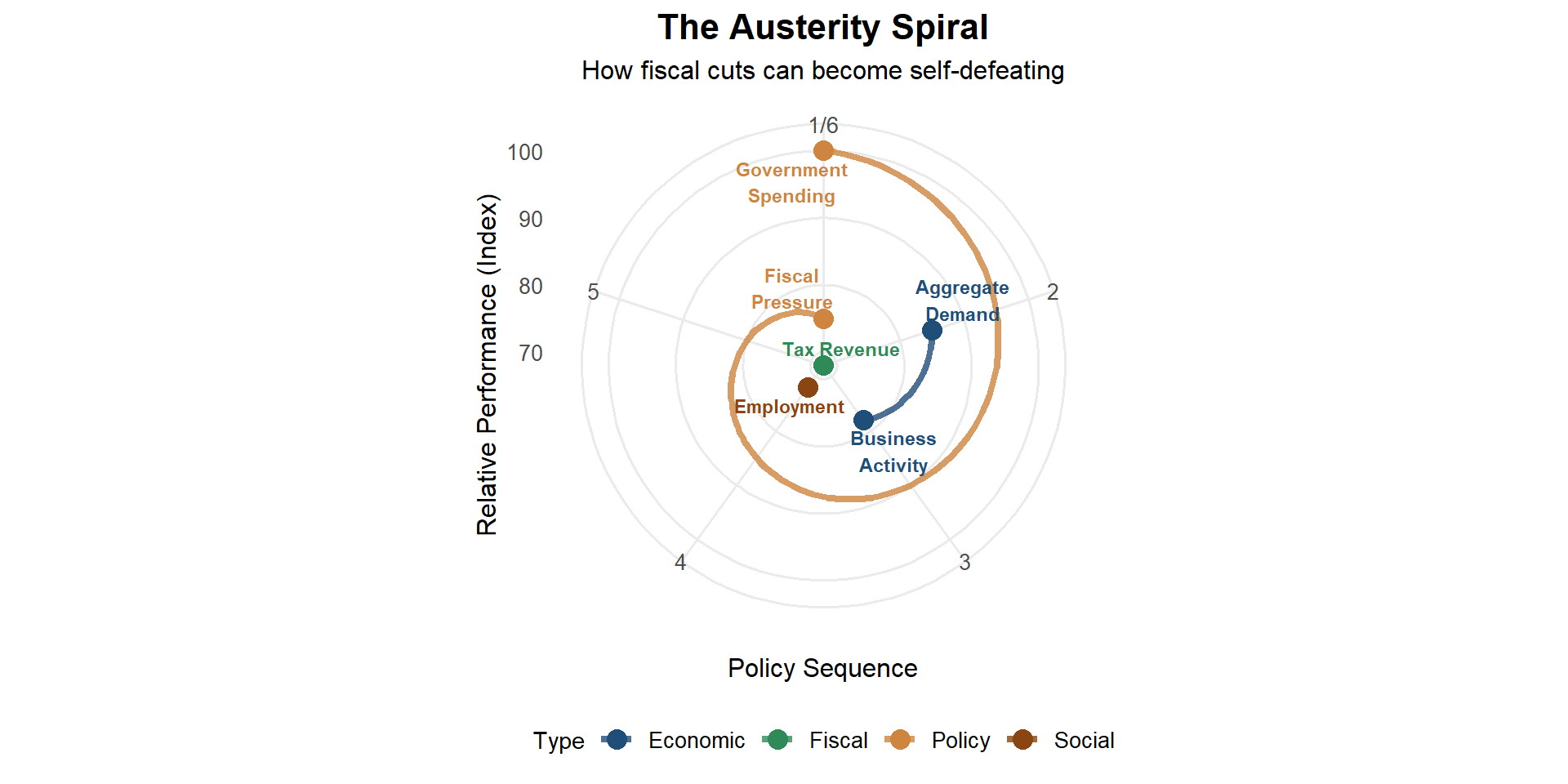

The Krugman Insight: When Austerity Becomes a Trap

“Austerity in a depression is a trap — the more you cut, the weaker your economy becomes.” — Paul Krugman

The Austerity Paradox Applied to Pakistan