If all series are non-stationary, use Johansen Cointegration procedure for case-3 option (constant in CE and in LR relation). Appropriate lag length selection is important.

Estimate VECM model and forecast it for next 4 quarters

Complete the write up and submit it in 1 hour.

• Experience the process of practical application of time series analysis.

• Get hands-on experience with the analysis of time series.

• Give correct interpretation of outcomes of the analysis.

Main Objectives

Concept of cointegration

Studying the dynamics of cointegrated variables

Methods for testing cointegration

How to estimate a system of cointegrated variables

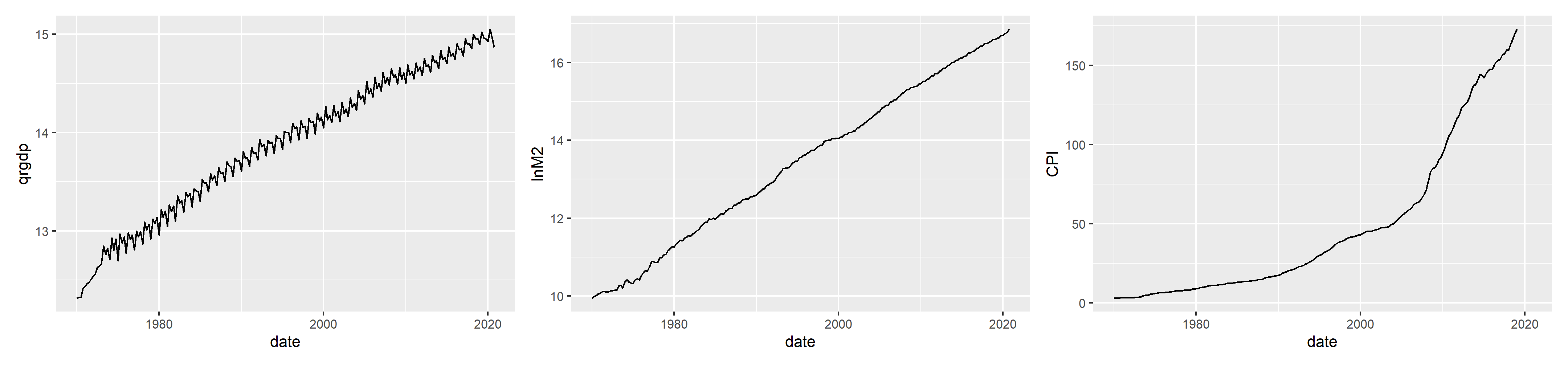

These graphs indicate all three variables are non-stationary.

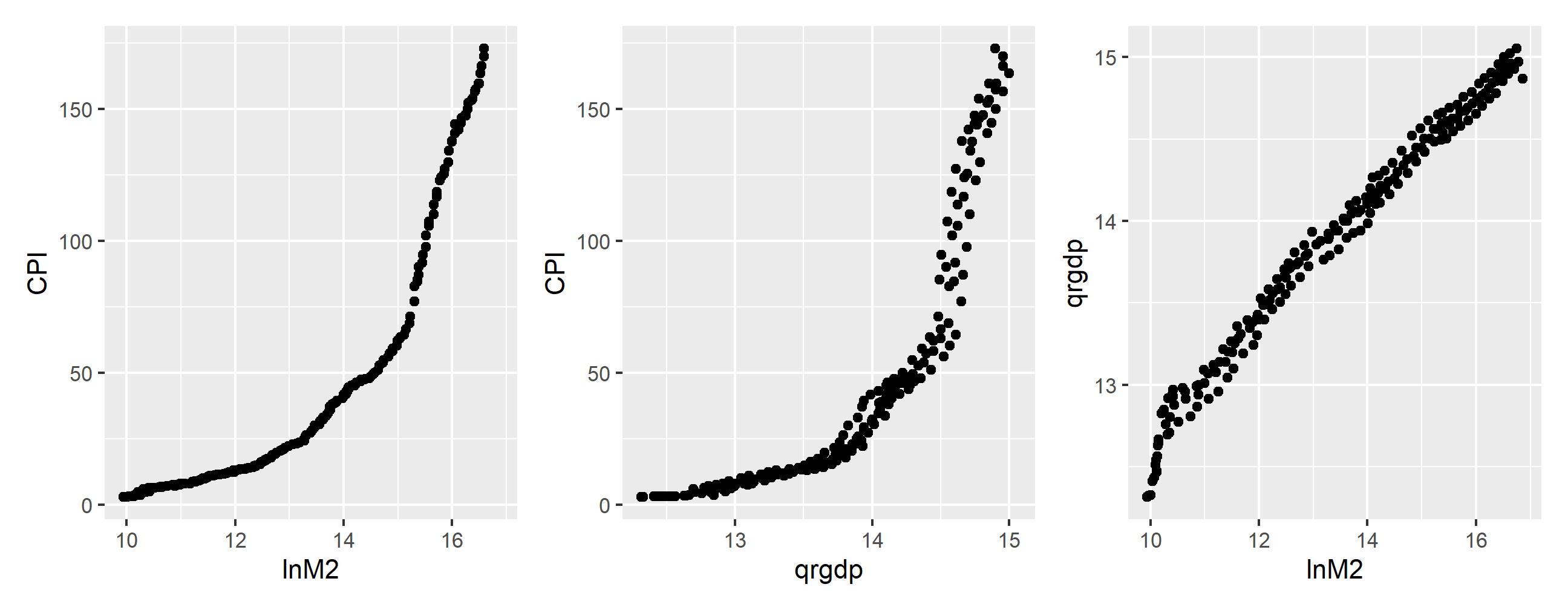

Scatter plot of the variables

Linear Combinations of I(1) series

In general a linear combination of I(1) series ) series is also I( 1).

However, in some special cases there could be a linear combination which is I(0).

So something very special has to happen for a linear combination to become stationary.

Intuition based on theory

Usually economic theory helps to find reason why linear combination of I(1) series is stationary I(0).

For example Permanent Income Hypothesis, Commodity Market Arbitrage, Purchasing Power Parity

Theory guides but one has to test it

What is Cointegration

I(1) series are cointegrated if there exists at least one linear combination of these variables which is I(0).

In our example _mpy_ if \(b_1m+b_2p+b_3y\) is stationary, there is cointegration.

In case variables are nonstationary, usual VAR not a good idea.

In case variables are nonstationary but cointegrated, VAR in difference form miss long run dynamics

In case variables are nonstationary, not cointegrated, then VAR in difference.

So lets elaborate more on cointegration and Vector Error Correction models.

Cointegretion and Vector Error Correction Model (VECM)

Money Market equiblibrium \(M^s=M^d=\beta_0+\beta_1p_t+\beta_2y_t+\beta_3r_t+e_t\)\(e_t\) is not persistent and its variance should not rise over time. If \(b_1m+b_2p+b_3y\) is stationary, it means despite each series being non-stationary, their linear combination is stationary and hence these variables are cointegrated.

Long run relationship If \(b_1m+b_2p+b_3y\) is stationary, it means there must be some adjustment made by m,p and y that move together such that deviation from \(b_1m+b_2p+b_3y\)=0 remains bounded.

Money and Price

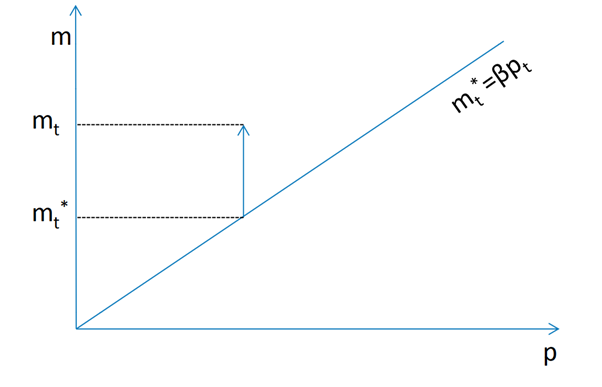

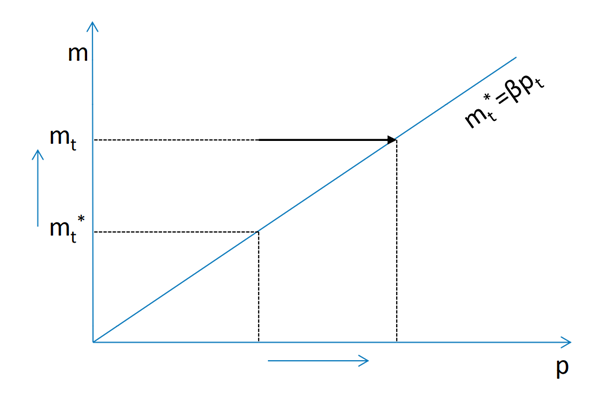

Suppose that in the long run \(m_t=\beta p_t+e_t\) where \(\beta>0\) That is \(m_t\) and \(p_t\) are cointegrated and money nuetrality hypothesis would imply \(\beta=1\). If \(m \uparrow\) s.t \(m_t-\beta p_t>0\), what would be the dynamics?

Deviation and now what

\(m_t\) is doing all the adjument

\(m^*_t\) is unchanged and \(m_t\)\(\downarrow\)

\(\Delta m_t=\alpha_m(m_{t-1}-m^*_{t-1})\) where \(\alpha_m<0\) Short run change in \(m_t\) is a linear function of the deviation from the long run from the long run equilibrium

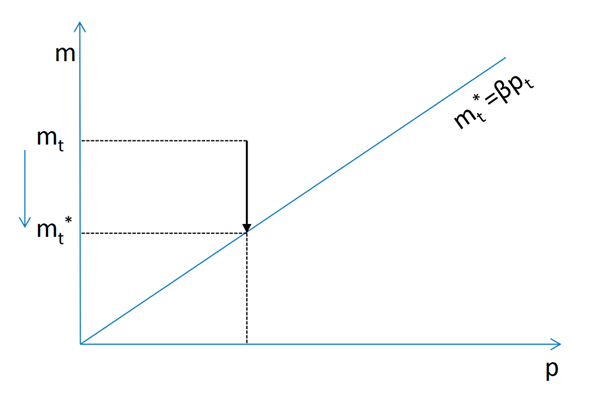

\(m^*_t\) is doing all the adjument

\(m_t\) is unchanged and \(p_t\) and \(m^*_t\)\(\uparrow\)\(\Delta p_t=\alpha_p(m_{t-1}-m^*_{t-1})\) where \(\alpha_p>0\) Short run change in \(p_t\) is a linear function of the deviation from the long run from the long run equilibrium

Both \(m_t\) and \(p_t\) adjust__

\(m_t\) and \(p_t\) are adjusting simultaneously \(\Delta m_t=\alpha_m(m_{t-1}-m^*_{t-1})\)\(\Delta p_t=\alpha_p(m_{t-1}-m^*_{t-1})\) which is basically error/equilibrium correction model. !…

Cointegration and VECM (Continued)

Simple ECM\(m_t\) and \(p_t\) are cointegrated with adjustment in \(e_t\)\(\Delta m_t=\alpha_m(m_{t-1}-\beta p_{t-1})+\nu_t\)\(\Delta p_t=\alpha_p(m_{t-1}-\beta p_{t-1})+\mu_t\) A VAR in difference would be misspecified.